Warren Buffett has always ridiculed people who invest in gold, calling it a worthless metal that is "dug out of the ground in Africa or somewhere else" and a way to "live in fear for a long time."

But this year he joined other investors, including the world's largest hedge fund Bridgewater Associates, who piled heavily into the asset during the latest gold rush, which helped push gold prices to record levels this summer.

In the 2nd quarter of 2021, Buffett's management company Berkshire Hathaway bought a stake in Barrick Gold, the world's second-largest gold miner, for $565 million. Shares of Barrick, which mines in Africa, Latin America and the United States, from early April to early October increased by 37%.

Bridgewater also invested $316 million in gold-backed exchange-traded funds in the second quarter, according to company filings.

Gold-backed funds, or simply gold exchange-traded funds , are exchange-traded funds (ETFs) whose assets are backed by gold and which allow investors to purchase physical gold as shares of the funds.

This interest from Western investors was driven by the rise in the price of gold from a low of $1,160 in the summer of 2021 to an all-time high of $2,073 per ounce in August 2021 , making the precious metal one of the best-performing financial assets in the world.

Growing concerns about the economic fallout from the coronavirus and negative bond yields have led to more than $60 billion being invested in gold-backed ETFs this year, up 50% since the 2009 financial crisis.

The pandemic has convinced investors that gold should be in their portfolios as a hedge against foaming stock markets, rock-bottom interest rates and falling output.

In stock exchange slang, a frothy market means very high and unstable quotes at the peak of a trend, which can lead to a sharp collapse.

Some major investors have moved assets into gold to protect against possible deflation caused by slowing economic growth as governments pump money into their economies, said David Tate, chief executive of the World Gold Council.

After an initial fall in March amid the collapse of global stock markets, gold rose by %22 by early August .

“It made a lot of people who had always looked at gold as an Armageddon asset take a broader look at it,” Tate says.

However, in the traditional eastern gold hubs of India and China, demand has been tepid at best this year , with buyers in the two largest consumer markets selling their gold holdings or borrowing against their gold holdings as prices hit record highs in local currencies .

In China, gold is selling at a discount of $53 per ounce to global markets due to weak domestic demand and restrictions on exports of the metal.

With retail consumption a key signal of the commodity's strength to institutional investors, the divergence could threaten sharp moves in the gold price if Western demand weakens, as happened after the financial crisis when gold prices fell from a high of $1,920 an ounce in September 2011 to almost $1,200 in 2013.

Gold ETFs now account for 35% of global gold demand, up from 8% a decade ago, but capital inflows have begun to slow.

The world's largest gold ETF, SPDR Gold Shares, recorded a withdrawal from the fund in September for the first time in 8 months.

An abrupt halt to gold's rise would hurt some of the world's biggest investors and remove one of the few bright spots in global stock markets other than big tech stocks.

It will also lead to losses for retail investors, who face labor market uncertainty due to the pandemic and continued low interest rates on savings accounts.

By early October 2021, gold prices had fallen 9% from their August high, and gold mining stocks had fallen 13%.

“One risky scenario here involves Asian buyers setting the floor [floor] for the market decline, which undermines the confidence of retail investors who have bought gold-backed ETFs,” says Adrian Ash, head of research at BullionVault, an online gold exchange. “But where will that floor be with demand so low in large consuming countries?”

Falling consumer demand for gold.

Popley Eternal, a jewelery megastore in the bustling area of India's financial capital Mumbai that has been in business for nearly 100 years, usually caters to a crowd of ordinary people buying gold necklaces and earrings ahead of weddings and festivals.

The cost of gold jewelry starts from 50,000 rupees ($680).

But footfall has not recovered to pre-pandemic levels since the store reopened in June following the lifting of the country's strict coronavirus lockdown.

The three-month lockdown stopped almost all economic activity. The store's owner, Suraj Popli, says the company has cut its workforce by about a quarter to 20 people, with sales so low that any gold jewelery sold in the current climate is considered a "bonus".

Instead, Indian consumers, hit by the economic fallout of the lockdown, are choosing to sell their heirloom jewels or borrow against them to make the most of high global gold prices.

“People come to the store to sell gold when they need money,” he says, “Very few people come to buy.”

India and China combined account for more than half of the world's gold purchases.

demand fell 56% in India and just over half in China in the first half of this year according to the World Gold Council , although demand in India picked up again in August.

In India, the precious metal plays an extremely important role in family, festive and religious matters. The South Asian country has the world's largest reserve of gold, with 25,000 tonnes owned by households and stored in temples .

Even for investment, many Indians have traditionally preferred to hoard physical metal rather than buy it in ETFs or other exchange-traded vehicles. Gold jewelry gives status and can be bequeathed to children and pawned in times of need.

“There is an emotional craving for gold,” says Terence Lucien, head of mutual funds at PhonePe, a Bengaluru-based e-payments startup owned by Walmart. “Traditionally, Indians buy it in abundance.”

But demand for jewelry has fallen, primarily due to a sharp lockdown that forced retail stores to close, as well as the pandemic's heavy blow to the economy and health care system.

To date, India has reported more than 5.8 million cases of coronavirus and more than 92,000 deaths.

Many weddings have been postponed as India records more than 80,000 new infections a day, while economic difficulties (GDP fell 24% in the three months to the end of June) have reduced the appetite for ostentatious spending.

Shekhar Bhandari, head of precious metals at Kotak Mahindra Bank, says he expects demand to rebound once the pandemic ends.

“Have weddings been postponed? The answer is yes,” he says. “Will marriage rates decrease in the long term? No".

Price pressure on gold.

The pandemic, however, has exposed a long-term decline in demand for physical gold in a country of 1.4 billion people, growing financial literacy and access to products such as mutual funds that previously prompted many to diversify their investments into assets other than the metal.

Consumer demand fell from an annual average of 900 tonnes between 2010 and 2015 to less than 700 tonnes last year, according to UBS.

Several government programs in recent years to redirect demand into more financially efficient assets, such as gold-backed bonds, have failed to stem the decline.

China has also suffered from a fall in jewelry purchases due to coronavirus restrictions and hesitancy to buy gold at high prices. According to the World Gold Council, in the first half of the year, demand in China reached its lowest level since 2007 and amounted to 152.2 tons.

The social and economic disruption caused by the pandemic could accelerate the decline in demand for physical gold in India and China, undermining a vital consumer base for investors around the world.

This year, gold bullion has been shipped from Asia to vaults in the US and London via refineries in Switzerland to support growing Western demand for gold ETFs.

But if Western demand slows, those volumes could begin to put downward pressure on the market price, said Jeremy East, a former Standard Chartered banker in Hong Kong.

“No gold is going into China this year and very little is going into India,” East adds. “That means the [Western] ETF guys need to keep buying it, [especially] if at the end of the year China and India are still will not restore demand... This gold must find its home somewhere. The market needs more money to continue to absorb this gold."

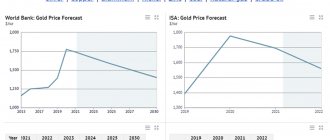

Gold Price Forecast 2021 – World Gold Council

Analysts at the World Gold Council (hereinafter referred to as analysts) believe that increasing uncertainty and problems with economic growth will stimulate demand for gold in 2020. In particular, analysts paid attention to several factors:

– financial uncertainty and low interest rates;

– weakening growth rates of the global economy;

– volatility of gold prices.

However, first let's look at history.

Gold really shines in 2021

Last year, the rate of the yellow metal showed the best result since 2010, rising in price by 18.4% in dollar terms. During this period, gold outpaced the world's main indicators for bonds and stocks on stock exchanges in developing countries in terms of its rate of return growth. In addition, the precious metal reached all-time highs in most major currencies except the dollar and the Swiss franc.

Gold rose in price the most in June-September due to increased uncertainty and lower interest rates. However, investor interest in the yellow metal has been strong throughout the year, as evidenced by gains in exchange-traded funds, increased buying by central banks and net long positions on the COMEX.

High level of risks and low interest rates

According to analysts, the dynamics of the global economy, which have formed over the past few years, will support the gold rate in 2021. In particular, we are talking about the following:

– financial and geopolitical uncertainty, combined with low interest rates, will likely ensure high levels of investment demand for gold;

– Aggregate purchases of the precious metal by central banks are expected to remain at a sustainable level, even if the figures are below the record highs observed in recent quarters;

– speculative positioning may lead to increased volatility in the gold price;

– volatility in the gold price, as well as the likelihood of reduced economic growth, may lead to lower demand for the precious metal from consumers in the short term, but structural economic reforms in India and China will support demand in the long term.

Favorable environment for investing in gold

In 2021, investors - including central banks - will face more new geopolitical challenges, while past conflicts will not be resolved, but simply relegated to the background. Additionally, low interest rates around the world will keep stock prices high. Investors will not abandon risky assets, but evidence suggests that demand for defensive assets to hedge portfolios is also increasing.

One of the key drivers of gold prices, especially in the short to medium term, is the opportunity cost of owning it compared to other assets such as short-term bonds. Unlike bonds, the yellow metal does not generate interest income or dividends because it has no credit risk. This perceived shortcoming may put off some investors. However, with a quarter of the government debt of developed countries trading at negative nominal rates (and if you look at these figures taking into account inflation, then it turns out that 90% of the debt is trading at negative real rates), the opportunity cost of gold ceases to be an issue, and its growth the exchange rate even provides some return compared to bonds. This is also confirmed by the strong positive correlation between the amount of debt and the price of the precious metal over the past four years. To some extent, this circumstance illustrates the distrust in fiat currencies due to the current monetary policy.

The low interest rate policy will continue for a long time. Many central banks - more than since the global financial crisis - are cutting rates, implementing quantitative (or quasi-quantitative) easing, and in some cases doing both.

It should be noted that the gold rate usually rises within 12-24 months after a change in monetary policy from tightening to easing. Now we are seeing something similar. When real rates are negative, gold's average monthly return is twice the long-term average. Even slightly positive real interest rates cannot lead to depreciation.

Gold price volatility may increase

Along with the rise in precious metal prices, their volatility has increased, but, compared to other assets, the latter remains below the long-term trend. According to forecasts, there will be no reduction in gold volatility in the near future. If the economic and political environment worsens, volatility will increase, given that this indicator tends to rise in such circumstances, especially when stock prices fall.

Decreased economic growth could negatively impact consumers

According to a survey of economists, positive growth will be observed in 2021 in most countries, but in 2021-2022, according to some, problems will be observed in leading countries. However, on average, forecasts indicate slight growth in the global economy this year compared to 2019. Considering also the volatility of the gold rate (at current levels or higher), jewelry consumers may reduce their purchases, and technology demand will also show a decline.

Chinese consumers' incomes are declining and their needs are changing

A slowdown in China's economic growth and rising prices for key consumer goods are reducing the amount of disposable spending among consumers. While (apparent) progress in trade negotiations with the US may restore some confidence, uncertainty remains.

With tight budgets and higher spending on basic consumer goods, consumption of luxury goods will decrease, meaning the jewelry market in China will also suffer. In addition, young consumers prefer to buy innovative jewelry with fashionable designs and lighter weight - the divergence in sales of traditional and innovative products may continue in 2021.

Price volatility and high taxes could turn Indian consumers away from the yellow metal

The Goods and Services Tax, introduced in India three years ago, was increased in many categories last year. In addition, the duty on gold imports increased from 10 to 12.5%. Until tax cuts are implemented as a reliable stimulus for economic growth (the corresponding infrastructure may not be ready until 2021), the current situation is exacerbating problems with gold consumption, coupled with record high domestic gold prices. The introduction of mandatory hallmark markings for gold jewelry earlier this year could boost consumer confidence. However, this innovation is likely to have a negative impact on the market at first.

Overall, consumer and gold market sentiment could deteriorate throughout 2021.

Economic reforms will increase demand for the precious metal in the long term

China and India are pursuing economic reforms aimed at strengthening growth and domestic consumption. China's One Belt, One Road project should strengthen the country's regional influence and reduce dependence on the West. Policy reforms in India to bring transparency and an orderly trade structure to many sectors of the economy can improve confidence and remove impediments to growth. These factors are forecast to have a long-term positive impact on the gold market, although this will only become apparent in the future.

The impact of supply and demand on the gold rate

The pricing of gold is different from the pricing of stocks and bonds. The precious metal does not pay dividends, so conventional discounted cash flow models cannot be applied to it. At the same time, the yellow metal has no expected earnings or book value.

Its dual nature—as a consumer good and an investment—means that demand for jewelry can be boosted by economic growth, even if investment demand declines due to reduced uncertainty or higher interest rates. This characteristic makes the yellow metal an effective strategic asset.

The equilibrium price of gold is determined by the interaction of supply and demand.

In particular, the dynamics of the precious metal exchange rate can be explained by four sets of factors:

– economic growth: periods of growth are very favorable for the jewelry market, technology development and long-term savings;

– risk and uncertainty: stock market downturns often increase investment demand for gold as a defensive asset;

– opportunity costs: the price of competing assets, especially bonds (due to interest rates), currencies and, to a lesser extent, other assets influences investor attitudes towards gold;

– investor attitudes: capital flows, positioning and price movements can increase or decrease the price of gold.

2020 will be a pretty good year overall for gold

The yellow metal rose 4% in December 2021, rising another 6% by January 7, 2021. This was mainly due to tensions in the Middle East associated with the confrontation between the United States and Iran.

Subsequent comments from US President Donald Trump eased tensions, lowering the price to US$1,550-$1,560 per ounce. Nevertheless, the gold rate exceeds the end of 2019 by 2.6%.

Investor positioning surrounding this particular event is expected to impact gold's performance in the near future. However, significant financial and geopolitical uncertainty will play a more important role in the medium term. Let's look at four different hypothetical macroeconomic scenarios provided by Oxford Economics:

– slowdown in global economic growth (their baseline scenario);

– economic recession that will begin in the United States;

– a more pronounced slowdown in economic growth in China;

– improving the economic situation in developing countries.

Overall, gold is expected to perform well in 2020. Although some of the scenarios - with the exception of economic recovery in developing countries - may lead to a decrease in consumer demand, which will negatively affect the gold rate. However, in this case, these consequences are offset by an increase in investment demand against the backdrop of deteriorating credit conditions and a stable decline in interest rates.

However, it is important to note that this is not a complete list of possible scenarios. These are key investor concerns identified in Oxford Economics' Global Risks Report. Therefore, hypothetically, an improvement in investor sentiment in the stock market, for example due to reduced risks and a low likelihood of further easing by the Fed or other major central banks, as well as tightening of monetary policy, but not through rates, could all have a negative impact to the gold rate.