Illustrative photo: Getty Images / Yevgeniy Sambulov Gold is one of the most popular investment instruments. And against the backdrop of a decline in its value, prospects for profitable investments arise. Read more in Nurfin's article.

The price of gold in 2021 fluctuated and depreciated from 26,128 tenge to 24,297 tenge per gram (January 1 – August 17), according to the National Bank.

The minimum price for this period was reached on March 9 – 22,862 tenge per gram.

At the same time, despite the general downward trend in prices, Kazakhstanis continued to actively buy gold.

Thus, in June 2021, a record number of gold bars were purchased - 3,188 units, the total weight of which is 124.2 kilograms.

According to the exchange telegram channel Tim Martynov, investing in gold can become justified and bring income in the medium term. However, we should not forget about the risks.

Gold price in 2021. Source: National Bank of Kazakhstan

Why did gold fall in price?

The decline in the value of gold was influenced not only by inflationary processes, but also by physical phenomena.

For example, one of the important reasons for the fall in the price of the precious metal was the increase in gold production in 2021. And in the first half of 2021, the production level reached 1,783 tons - 9% more than a year earlier.

As a result, supply on the world market increased, which was reflected in prices.

The second important reason that influenced the gold rate was the worsening situation with COVID-19 in India, one of the largest buyers of gold products.

As a result, the Indian jewelry industry was suspended.

And demand for gold in the jewelry manufacturing sector fell from 63% to 41% of total demand in the second quarter of 2021. That is, only 391 tons of 955 tons of production were purchased.

For comparison, in the previous 5 years, the Indian jewelry industry purchased about 873 tons of gold annually in the first 6 months.

Illustrative photo: Freepik

Dollars, real estate, gold: an analyst explained where it is better to invest money

— A bank deposit is the most popular and understandable way for most Russians to save their own money. Is it suitable for these purposes today?

— The chances of earning even a little money with bank deposits today are almost zero. It’s just that the current interest rates in banks on average do not even cover the official increase in inflation published by Rosstat.

The relationship between return on deposits and inflation is like in the ancient philosophical paradox about Achilles and the tortoise. Fast Achilles cannot catch up with her. While he runs the distance to the turtle, it moves forward. He again overcomes the path to her, but during this time she crawls further again. And so on ad infinitum.

The same is true with bank deposits: according to the Central Bank, the average rate on ruble deposits of the 10 largest banks in September increased to 6.33%. After the Central Bank increases the key rate in October from 6.75% to 7.5%, the yield on such deposits may increase to 7-7.2%. At the same time, the inflation rate in the first month of autumn was 7.4%. In October it is expected to increase to 8%. And this is only according to official data from Rosstat. And if we count the real price increases recorded by people “for themselves,” the gap will be even greater. The Central Bank of the Russian Federation claims that the inflation observed by Russians in September was at the level of 12.5%.

— But by the end of the year, inflation is predicted to slow down. Perhaps, if the deposit is opened for a long time, then it will still be possible to protect the funds from rising prices?

— The Bank of Russia does not expect a noticeable slowdown in inflation by the end of the year. Its forecast for 2021 was raised in October to 7.4-7.9% from previous expectations of 5.7-6.2%. But according to the regulator’s assumptions, in 2022 its official level may actually drop to 4-4.5%.

However, given the ease with which the Central Bank revises forecasts, there is a possibility that this figure will be exceeded. Accordingly, if you place bank deposits at the interest rates offered today for a period of a year or more, then there is a chance to compensate for inflation during this period based on the results of the entire period. However, it is still difficult to talk about earnings in such a situation.

The main advantage of bank deposits is their reliability. Deposits of individuals in the amount of up to 1.4 million rubles are protected by an insurance system. 90% of deposits do not exceed this amount.

If a person’s volume of such investments is above this level, then it is better to distribute it among several banks. You also need to remember that from 2021 a tax has been introduced for individuals on income from deposits. It is equal to 13% of the excess of all interest received during the year on deposits over the amount of 1 million rubles, multiplied by the rate of the Central Bank of the Russian Federation as of January 1.

By the way, if you have savings, this is already considerable luck. After all, according to statistics, 37% of Russians have no savings at all. If you belong to these lucky ones and have funds that you want not only to save from inflation, but also to increase, then placing money in bank deposits is not enough. Popular wisdom advises not to put all your eggs in one basket. In financial language, this means a simple rule: diversify your investment portfolio, that is, distribute your investments in several areas. You can put some of your personal capital in the bank, but consider other financial instruments.

— The next favorite option for saving money from citizens is buying foreign currency. Is the strategy “In any unclear situation, buy dollars or euros” still relevant?

— The ruble lost its reputation in numerous crises and disasters, after which it depreciated in leaps and bounds. Hypothetically, even now there are risks of its sharp weakening to levels above 75-76 rubles per dollar. This is possible in case of some unforeseen circumstances. For example, with the intensification of new waves of the pandemic, increasing geopolitical risks, and tightening anti-Russian sanctions in the United States.

However, given the current realities, a sharp weakening of the ruble is still unlikely. This is hampered by high prices for oil and gas, large international reserves of Russia, low public debt, surplus budget, trade and payments balances of our country.

The Central Bank's key rate continues to increase, which, according to its forecasts, could average 7.3 - 8.3% in 2022. This contributes to the attractiveness of ruble assets for investors. At the same time, much will depend on the position of the US Federal Reserve. The Federal Reserve is expected to announce in November that it will reduce its cash injections into the economy in the coming months, and may raise its interest rate in 2022. This would increase the dollar exchange rate and would be a blow to the prices of raw materials and the ruble.

— What will the dollar and euro exchange rates be by the end of the year, according to your forecasts?

— By the end of December, the exchange rate of the “American” against the ruble may rise to 72 rubles or higher, depending on the position of the Fed and energy prices. And if it does decline, which has been the case for the last month, then, obviously, no further than 68-70 rubles per dollar. After all, an excessively strong ruble is extremely unprofitable for large exporting companies and the Russian budget.

Next year, the dollar is more likely to move upward compared to the current rate due to its expected strengthening in the world as the policies of the American regulator tighten. The dollar may rise to 74-75 rubles. Considering that the exchange rate to the ruble is now favorable, it makes sense to partially convert free rubles into them.

In the longer term, there will be a long-term trend of strengthening of the leading currencies against the ruble. It is associated, first of all, with the general weakness of the Russian economy relative to developed countries, therefore, “with a long-term view,” investing part of one’s savings in dollars and euros is rational. There is a reason to purchase dollars and euros in approximately equal proportions and as insurance against “black swans” - unforeseen adverse events. But it is better not to limit yourself to this investment option, but to pay attention to less common types of financial investments.

Photo: pixabay.com

— Do you mean trading on the stock market?

— Yes, the Russians have “tried” this type of investment. In October 2021, the Moscow Exchange stated that the number of people with brokerage accounts on it “has increased by 6.2 million people since the beginning of 2021 and reached 15 million.” And although not all of them are active in transactions, the dynamics are convincing. Over ten months of the year, this amount increased by 70% of the “accumulated” amount over the entire existence of the exchange.

This happens, first of all, due to the above-described impossibility of Achilles’s deposits to keep up with the “turtle”, that is, to outpace inflation, and also due to the impressive growth in stock prices. For example, the Moscow Exchange index rose by about 26% only from January to October this year. Shares of American companies, many of which are available on the Moscow Exchange or through Russian and foreign brokers, also rose sharply in price. The S&P500 index grew by 22% per annum during this period. Much more than Russian inflation!

Demand is also supported by the fact that access to this market is very simplified. Any Russian who wants to invest even a small amount, starting from several thousand rubles, can open a brokerage account online through a bank or financial company and gain access to the exchange.

— What securities attract the interest of private investors?

— People buy more Russian government and corporate bonds than company shares. For a novice investor, the choice is rational. As the Central Bank's key rate rises, the yield on government bonds, for example, federal loan bonds (OFZ), also rises. They are also guaranteed by the state, regardless of the amount, unlike bank deposits. Now the yield on OFZ is about 7% per annum, that is, higher than on deposits.

It is important to monitor the situation here. After all, if inflation, according to the forecast of the Central Bank of the Russian Federation, begins to decline in 2022, then both the Bank of Russia rate and the interest on bonds will decrease. But if you buy them now, you can “stake out” the current higher yield for a long time. And in the event of a likely decrease in inflation, for example, to 5%, the investor will continue to receive about 7%. Moreover, when market yields fall, bond prices tend to rise. Therefore, the investor will be able to receive income not only from coupons, but also due to the rise in price of the securities themselves.

However, you need to remember that income on all bonds from January 1, 2021 is subject to personal income tax.

— What can you say about shares: is it profitable to buy them today?

— The highest returns can come from active investments in more volatile, that is, instruments that change in price. A classic example is stocks. We have already noted their growth, which is many times faster than inflation. It is also worth considering collective investment funds with diversified investments - exchange traded funds ETF (from the English exchange traded fund - exchange-traded investment fund), mutual investment funds (UIFs).

But the rise in stock prices over the 10 months of this year now does not reduce, but rather increases the risks. As the saying goes: “The higher, the more breathtaking.” The rise in stock indices is largely due to the euphoria of the gradual recovery from the pandemic, with large-scale “infusions” of money by global central banks, primarily the US Federal Reserve, to stimulate the economy.

Such a powerful rise is far removed from the recovery growth of the real sector and is artificial and speculative in nature. This increasingly makes us talk about a “bubble”, “overheating” of the market. It is very likely that there will be a significant correctional decline in the Moscow Exchange, S&P500 and other indices in the near future. Perhaps it is worth focusing not only on the growth of stock prices, but also on dividend payments. It is better for a non-specialist to rely on professionals in this matter.

Photo: Alexey Moshchenkov

— Let's continue the conversation about classic options for saving funds. Does investing in real estate or buying a home for investment purposes make sense in the current conditions?

— Russians who have sufficient savings often consider investing in real estate as an investment, often with the purpose of renting it out. Renting a home, for example, can bring 4-5% per year including taxes. At the same time, the price of real estate itself in the long term grows, as a rule, no less than general inflation, even if it dips briefly in some periods.

In this area, price dynamics over the past year, as in stocks, are completely different from the crisis. For example, in Moscow, the average price of a meter of housing rose in September 2021 to 236 thousand rubles. from 187 thousand rubles. a year earlier, that is, by 26%, according to the Real Estate Market Indicators (RIM) service. In the Moscow region, the growth during this period was even higher - up to 130 thousand rubles. from 98 thousand rubles, that is, by 32%. Housing outperformed stock returns.

— It turns out that investing in square meters is still profitable?

— Here you need to be careful, as with stocks: now the market is at its peak. Investments in real estate for investment purposes are hardly advisable. Many factors of price growth that made it abnormal are disappearing, such as the flow of funds here from deposits and “from under mattresses”, low interest rates on mortgages, especially with government benefits, relatively reasonable housing prices, growing inflation, etc. Demand is extremely limited by household incomes, which are in no hurry to grow.

The increase in the key rate of the Central Bank of the Russian Federation, favorable for deposits, turns its back on mortgages and real estate prices. Thus, the average rate on residential mortgage loans as of September 2021 was 7.26%, and as of September 2021 – already 7.78%, according to the Bank of Russia. After the Central Bank's key rate increases in October, these percentages will become even higher. Therefore, purchasing real estate with a mortgage to generate income at current prices is a completely losing option.

— What other tools can citizens consider to save their money?

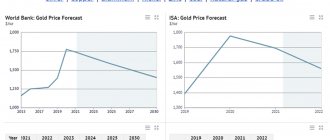

- Gold. As an investment object, it traditionally acts as a “defensive” asset against inflation, economic tension and other troubles. For example, over the past three years, since June 2021, the precious metal has risen in price from 1230 to 1780 dollars per troy ounce, that is, by 45%. Moreover, in August 2020 the price reached $2,120. From such a position, it makes sense, in principle, to consider these investments as long-term - for a future of 3 to 5 years.

— Is it worth investing in gold now? After all, like other financial assets, it has its drawbacks, doesn’t it?

— Gold can be purchased in different ways. For example, buy “live” ingots in banks – real pieces of metal. This may be an alternative to foreign currency deposits. In addition, a gold bar is a real, tangible thing, a source of pride. You could say that you are part of the “caste of society.” But in practice, such investments are unprofitable. Particularly due to taxes. A person buys bullion from a bank and pays 20% VAT. And when he wants to sell, these tax payments are not returned to him. In addition, bullion also requires storage costs, there are risks of loss and damage...

— What alternatives are there to bullion?

— Unallocated metal accounts (OMA) do not have the listed disadvantages. That is, you don’t buy “real” gold, but you put money for this amount into your compulsory medical insurance account at the bank. For example, gold now costs approximately $1,780 per ounce. If it rises in price and then reaches 1900, then when closing the account the investor receives an amount already at this price of gold.

But there are negative nuances here too. Indeed, on such accounts, unlike deposits, practically no interest is accrued. They are not included in the deposit insurance system, that is, their return is not guaranteed by the state in the event of bank bankruptcy. In any case, you need to consider the risks. The price of the precious metal may fall. At the right moment for the investor, the value of the asset may be lower than when investing in it.

How much will a 999 gold bar cost in Sberbank for 1 kg in 2021

What is the reason for the growing popularity of purchasing an asset such as gold?

The fact is that its price is steadily growing. It is worth investing in gold for the following reasons: • metal production in Russia exceeds that of other countries; • its price is rising all the time.

Thus, buying precious metals is a profitable investment. A bank client has the right to purchase and sell gold whenever he needs it.

Quotes are constantly changing; it is impossible to know the current price in advance.

According to the latest information, the price for 1 kilogram of 999-carat gold is 2,853,823 rubles.