Content

- Gold and inflation

- Gold production and consumption

- Gold price and risk-free return

- Current situation in the gold market

- The role of gold for the Russian economy

Anton Tabakh, Managing Director for Macroeconomic Analysis and Forecasting, Expert RA

Anton Prokudin, leading methodologist at Expert RA

Gold and other precious metals have always been safe haven assets for investors in times of crisis. And the new crisis caused by the COVID-19 epidemic is accompanied by rising gold prices. The world's central banks and simply large banks have intensified their purchases of gold against the backdrop of rising risks and lower interest rates in both developed and developing countries. At the same time, the price of gold has been growing over the past 1.5 years; before that, it was stably quoted at $1,100–1,300 per ounce.

For Russia, the price of gold is an important macroeconomic factor: firstly, the gold mining industry plays an important role in the trade balance and mineral extraction tax (although it is significantly inferior to the oil and gas industry). Secondly, Russian international reserves have a higher share of gold than the average of countries that do not issue reserve currencies, that is, those that need reserves as protection against potential sanctions. In recent years, this has contributed to the revaluation of reserves, but if prices fall, there is a threat of a double hit - both in revenues and in reserves.

Gold production has been steadily increasing, and demand for it from regular sources peaked 20 years ago, so the market balance is tilting towards a surplus of gold. The increase in gold prices in 2000–2011 was not accompanied by an increase in constant demand; on the contrary, it even decreased. Variable (investment) demand has pushed up gold prices, especially since 2006, and it is thanks to it that the price of gold remains high today. The reason for the high investment demand lies in the dynamics of real interest rates, which have been declining in recent years and are moving into negative territory in 2020.

As economies recover and Western central bank monetary policies normalize, variable demand for gold will reverse and the price may decline significantly, but normalization may take a longer period than in previous cycles. Against this background, the likelihood of continued high gold prices in the medium term is very high, as is the possibility of accumulation of risks for investors and central banks.

At the same time, along with gold, other precious metals also act as a hedge against inflation. Buying the cheapest of them (currently platinum) will protect the investor from unnecessary losses over a long time horizon.

Current situation.

In 2014, Russia's gold and foreign currency reserves fell from $500 billion to $385 billion. – funds were spent on currency issues during periods of depreciation of the ruble. Many experts are still arguing whether this should have been done, because there was no effect - the devaluation of the ruble was 100%. Others argue that if the Central Bank had not done this, then the fall would have been even greater (more than 200%), and the economy would have suffered significant losses. This year already promises to be no less difficult. Whether the gold and foreign currency reserves will have to be lowered again in order to support the national currency remains in question.

Author of the article, financial expert

Dmitry Tachkov

Hello, I am the author of this article. I have a higher education. Qualified investor. Finance and credit specialist. Worked in commercial banks of the Russian Federation for more than 3 years. I have been writing about finance for more than 5 years. Please rate my article, this will help improve it.

about the author

Useless

3

Interesting

3

Helped

14

Gold and inflation

Gold (along with silver) has been the main means of payment for hundreds of years and circulated in the form of coins in the economies of most countries of the world. In the 19th and early 20th centuries, gold and silver were in circulation in parallel with paper money issued by private banks, and in 1944–1971, the gold exchange standard (Bretton Woods system) was in force in the world, when central banks had US dollars in reserves, and The US gold reserves provided dollars. After 1971, gold ceased to be used as collateral by Western countries, and the era of fiat money began.

Over the past centuries, the United States and other countries have experienced inflationary spikes due to wars and various economic disasters, but usually reverted back to a fixed rate against gold. At the same time, the stability of the banking system depended on the presence of sufficient reserves of specie in reserves: in the second half of the 19th century, the normal ratio between gold and issued bank notes was 15%. Therefore, the barometer of the health of the financial system was the ratio between the money supply or GDP 1 and the stock of gold (and sometimes silver) in banks. Nowadays, such accurate reporting is not maintained, so you can start from the ratio of GDP or money supply to all gold mined in the world. Considering that the volume of money supply in developed countries, using the example of the United States, is usually 60% of GDP, the reserve ratio to GDP would be 9%.

Chart 1 clearly shows that the cost of all mined gold (and silver) 2 compared to GDP was high in the 1930s (after Roosevelt artificially increased the price of gold), at the turn of the 1970s and 1980s (due to soaring inflation and losses confidence in currencies after the abolition of the Bretton Woods system in 1971) and this year against the backdrop of a pandemic and crisis. In quiet times, the valuation of all gold and silver mined falls to 5% of GDP, as it did in the late 1960s and 1990s.

If we look at the US economy since 1900 and the level of inflation in it, it becomes obvious that after the abolition of the Bretton Woods system, high inflation accompanied the rise in the price of gold, but the high price of gold is now observed against the backdrop of low inflation. Therefore, the reason for the price increase is likely to be not only high inflation. During the period of the gold or gold exchange standard in the United States, high inflation was perceived as a temporary phenomenon, followed by a rollback of prices, and only in the 1950s it became clear that inflation could be permanent, which is why the phenomenon of rising gold prices with an inflationary surge until the middle of the 20th century century was not observed.

The prices of silver and other metals are not as closely linked to investment cycles, so their high prices may not coincide with gold's peaks. For comparison, Chart 3 shows the prices of silver, platinum and palladium relative to inflation in the United States. It can be clearly seen that silver was at its peak in 1980, palladium in 2000 and 2020, and platinum prices are more relaxed and were expensive in 1980 and 2008-2010.

When choosing between precious metals today, we can say with confidence that:

- gold is expensive by historical standards;

- palladium is the most expensive of the precious metals, and its price has the prospect of falling sharply;

- platinum is the cheapest of these metals,

Therefore, it is now more profitable for investors to choose platinum rather than gold as a protective asset. Prices for all of the precious metals listed rise over a long time horizon along with inflation, so they are equally suitable for protecting savings from inflation.

Gold reserves

The gold and foreign exchange reserves of a single state are not only reserves of precious metals, but also debt obligations of foreign companies and foreign currencies in the form of cash. Reserves are used by the government of the state to maintain a stable exchange rate in the country, as well as to ensure a number of other external obligations.

Gold and foreign exchange reserves are generally characterized by a high level of liquidity, due to which they can be used at any time to pay debts, invest, conduct trade transactions or for the purpose of the country's participation in global financial transactions.

Gold production and consumption

Gold production grew over the centuries along with the need for money, but even after the abolition of its circulation in the world, the attitude towards this product as a means of saving remained (the logic of Gresham’s law is clearly visible here), so gold production continued to grow and is at a record level according to the results of 2019.

Gold production, as will be shown below, completely covers the needs of industry. The second constant source of gold is scrap. Mining volumes are also increasing, rising from 20 million ounces in the early 1990s to 40 million ounces in recent years. In 2019, the supply of gold from permanent sources (mining and scrap) amounted to 150 million ounces per year.

If prices remain at $1,000–2,000, production volumes will remain at the current level or even increase, since the average production cost is much lower. The cost of gold production has risen substantially in line with the price over the past 20 years. At the same time, at the end of the 1990s it is clear that when the price of gold falls, the cost of production also falls due to the cessation of production at costly deposits.

Costs of $700 in recent years clearly indicate a large margin for a decline in the price of gold. The offer will remain high even at $700.

The constant demand for gold consists of its industrial consumption: mainly jewelry production, also the electronics industry, coin production. Industrial consumption of gold grew until the late 1990s amid a decline in its real price. Maximum demand was 120 million ounces per year. Further, consumption decreased due to rising prices. A decline was also observed in the late 1970s with surges in gold prices. It is obvious that gold prices can only receive support from industry at values of $400–1,000.

The market balance consists of the constant supply of gold minus its industrial consumption. Investment demand and demand from central banks can have either a negative or a positive balance and are therefore ignored in Chart 7.

The balance sheet shows that low gold prices in the late 1990s were accompanied by a lack of production, and since 2006 there has been a constant surplus of gold on the market amid high prices. Investment demand and demand from central banks was negative in the 1990s, and in the last 10 years it has been absorbing 40-60 million ounces per year. When investor interest shifts to other investments, the price of gold could fall quite sharply in the direction of $500-800 per ounce, where supply will decrease and demand will increase.

Requirements for the size of gold and currency reserves

The maximum size of gold reserves is not limited. But there are requirements for the minimum size of gold and foreign exchange reserves. The minimum size of gold and currency reserves is determined by the following requirements:

- Not less than 3 months import costs. The average values for the last 12 months are taken;

- According to the Guidotti criterion: not less than the amount of external debt payments over the next 12 months;

- According to Reddy's criterion. The sum of the previous two requirements is taken;

Emerging Economies The IMF uses the ARA EM composite indicator:

ARA EM = 150% × (0.05 × FE + 0.05 × M2 + 0.30 × ID + 0.15 × DPO)

Where:

- FE – export financing for the last 12 months;

- M2 – indicator of broad money supply;

- VD – the amount of payments on external debt for the next 12 months;

- LPO – the amount of long-term portfolio liabilities;

Gold price and risk-free return

Investment demand for gold is associated primarily with economic conditions, namely with real interest rates on government debt. In the absence of the opportunity to obtain a positive risk-free return, investors turn to a protective asset (gold). So historically, when real yields are very low, which happens in two combinations of yields and inflation, gold prices have risen. With a stable yield situation, gold was not in demand.

High gold prices are associated with the situation in financial markets, which do not allow investors to earn returns above the inflation rate, which leads to the flow of funds into protective assets (primarily gold). At the same time, gold production far exceeds constant demand at current prices, and a change in central bank policies to a more stringent one will lead to a flow of investors back from protective assets to risky ones. The price of gold will drop significantly.

Why are gold and foreign currency reserves needed?

Gold and foreign exchange reserves reflect the country's solvency and give it the opportunity to use the national currency, linked through interbank payment systems (SWIFT).

Gold and foreign exchange reserves are not just a financial cushion for the state for a rainy day. These reserves are the main asset of the Central Bank. Based on their size, the Central Bank can perform the following functions:

- Issue national currency;

- Cover the state budget deficit;

- Issue loans to banks;

- Pay for foreign contracts in foreign currency;

- Conduct monetary interventions in the foreign exchange market;

Gold and foreign exchange reserves indirectly support a stable exchange rate of the national currency, since a large amount of assets is a guarantee that the state will be able to fulfill its loan obligations to pay off debts. Gold and foreign exchange reserves influence the exchange rate not directly, but by increasing confidence in the state on the part of international investors. The same attitude can be found in any relationship. For example, a bank is not willing to lend to people who do not have any property or assets.

Gold and foreign exchange reserves are NOT used for:

- Investments in the construction of infrastructure facilities;

- Firefighting and disaster relief;

The only way to reduce the amount in gold reserves is to spend more than you earn. For example, have a constant state budget deficit.

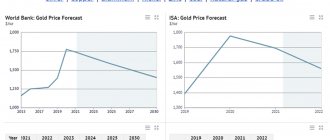

Current situation in the gold market

In 2021, the economic crisis caused by the COVID-19 pandemic has moved gold into the category of the main investment hedging assets. The high level of uncertainty and extra-loose monetary policies of the central banks of developed countries have exerted serious upward pressure on the level of gold prices, in some currencies the price of gold has reached record levels. According to the results of the first half of the year, the yield of gold at 17% exceeded the yield of all major global assets - the NASDAQ, S&P500 indices, American treasury bonds, not to mention oil.

In the first half of 2021, there was a drop in demand for physical gold (including coins and bars) by 6% compared to the first half of 2021. Demand from the electronics industry fell by 14%, and from the dental sector by 30%. Demand for jewelry fell by 39% in the first half of the year due to restrictions on economic activity. Central banks also reduced demand for gold - by 39% compared to the first half of 2019.

Gold supply also fell by 6% in the first half of 2021 due to a drop in production due to lockdowns and restrictions on economic activity.

First of all, the rise in the price of gold ensured a significant increase in flows into gold ETFs. In the first quarter, capital inflows into gold ETFs amounted to 16.6%; in the second quarter, the growth rate accelerated to 27%.

In the second quarter of 2021, rising gold prices supported an increasing level of uncertainty - the likelihood of a V-recession fell with the spread of coronavirus, and U- and W-variants of recession became more likely. Central banks of developed and a significant part of developing countries expanded their easing monetary policy measures: in addition to the almost traditional quantitative easing, programs for the purchase of corporate assets were announced. In addition, rising gold prices in the first quarter played a role.

In the third quarter, growth in inflows into gold ETFs slowed to 14.5%, likely due to the slowdown in gold price growth at the end of the third quarter. Despite the slowdown in price growth, the main factors that ensured the rise in gold prices in the first half of the year remain: uncertainty regarding the COVID-19 pandemic, soft policies of central banks. In addition, a supporting factor for gold prices was the Federal Reserve's statement about the possibility of inflation exceeding the 2% target without retaliatory action.

The role of gold for the Russian economy

Export

Russia is a net exporter of gold, and in 2019–2020 gold exports increased both in quantity and in value terms. In 2021, gold exports increased more than seven times in physical volume and more than eight times in value terms compared to 2018. The main buyer was Great Britain - the country bought gold for $5.33 billion out of $5.75 billion sold. A number of experts attribute the record demand for gold to uncertainty regarding Brexit. However, it should be remembered that the UK is the largest financial center, so a significant part of the flows can pass through it in transit.

Since the second quarter of 2021, gold exports have increased again - peak exports in April amounted to 42.5 tons, during April - June Russia exported approximately 24 tons of gold per month. The increase in gold exports in April 2021, which made it possible to at least slightly compensate for the fall in total exports of the Russian Federation, is associated with three main factors.

- In April 2021, the rules for exporting gold abroad changed in Russia: gold mining and refining companies were given the right to obtain general (and not one-time) licenses for exporting gold abroad. Previously, it was supposed to sell gold to banks lending companies, and the banks, in turn, had similar general licenses. Gold mining and refining companies could previously obtain one-time licenses to export gold, but this was associated with significant additional costs.

- On April 1, 2021, the Central Bank of the Russian Federation announced the suspension of gold purchases to fill gold and foreign exchange reserves. In fact, purchase volume has declined since the start of 2021. The policy of the Central Bank of the Russian Federation regarding the accumulation of gold and foreign exchange reserves will be discussed in more detail in the next section.

- At the end of March 2021, amid the uncertainty associated with the COVID-19 pandemic, concerns arose in the market regarding a physical shortage of gold on the New York Mercantile Exchange (COMEX). Concerns were triggered by an increase in the number of deliverable contracts, as well as an increased difference between the prices of futures on the American exchange and spot contracts in Europe.

The share of gold in the total exports of the Russian Federation is relatively small and until the end of 2019 amounted to a fraction of a percent. For comparison: the share of crude oil exports in total Russian exports until 2021 was about 30% (in the second quarter of 2021 it decreased to 20% due to falling oil prices). However, at the end of 2019 and in the second quarter of 2020, there was a significant increase in connection with the events described above; the share of gold in exports in the second quarter of 2021 increased to almost 7%.

It is likely that a similar share of gold in Russian exports will remain against the backdrop of relatively high gold prices and low oil prices, as well as uncertainty due to the COVID-19 pandemic.

Tax revenues from gold mining

Gold mining is subject to natural resource extraction tax (MET). Mineral extraction tax is a direct federal tax, so its changes are reflected in the revenue side of the federal budget. In general, the tax rate for gold is 6%, the tax base is the cost of the extracted mineral (concentrate or other semi-product containing gold).

In recent years, the cost of mined gold has remained at approximately the same level, despite fluctuations in the amount of the product mined, similarly, the amount of mineral extraction tax paid has remained at the same level - in the amount of about 4–4.5% (the percentage below 6 is due to cases of special taxation). For example, in 2021, Russian gold mining produced 747 billion rubles worth of product, which brought 34 billion rubles of mineral extraction tax to the treasury.

The share of taxes on gold mining occupies a small part of the revenues of the federal budget of the Russian Federation. For example, in 2021, the share of the mineral extraction tax on gold was about 0.56%, while almost 96% was the tax on the extraction of crude oil and natural gas. Despite the relatively constant absolute amount of mineral extraction tax paid for gold, the share of this tax in federal budget revenues has been declining over the past few years.

It is likely that based on the results of 2021, it will be possible to observe an increase in the share of gold taxes in the budget due to the increase in the cost of this precious metal and a decrease in oil prices.

Among the Russian regions for gold mining, one can distinguish the Republic of Sakha (Yakutia), Krasnoyarsk, Khabarovsk and Transbaikal territories, Amur, Irkutsk and Magadan regions, as well as Chukotka Autonomous Okrug. Together, these regions produce almost 90% of Russian gold in value terms.

The leader in the value of mined gold in 2021 (as in the previous few years) was the Krasnoyarsk Territory, where gold was mined for 160 billion rubles in value terms.

In accordance with accrued taxes, gold is the central natural resource for the Khabarovsk Territory, as well as the Amur and Magadan regions.

Table 1. Share of mineral extraction tax for gold in the total accrued mineral extraction tax by region, 2021

| Region | Mineral extraction tax for gold, billion rubles. | Mineral extraction tax for the region as a whole, billion rubles. | Share of mineral extraction tax for gold in the mineral extraction tax for the region as a whole, % |

| The Republic of Sakha (Yakutia) | 3,87 | 144,14 | 3 |

| Krasnoyarsk region | 9,29 | 273,62 | 3 |

| Khabarovsk region | 2,92 | 3,94 | 74 |

| Amur region | 2,19 | 2,55 | 86 |

| Irkutsk region | 2,72 | 173,42 | 2 |

| Magadan Region | 3,66 | 5,14 | 71 |

| Transbaikal region | 2,21 | 43,07 | 5 |

| Chukotka Autonomous Okrug | 3,22 | 15,10 | 21 |

Source: calculated based on Federal Tax Service data

Another source of federal budget revenue is taxes on jewelry manufacturers.

Gold and foreign exchange reserves of countries

For several years now, China has held the palm in terms of the volume of gold and foreign exchange reserves, which, according to the most conservative estimates, have already exceeded $3.5 trillion. Among the closest contenders for first place are Switzerland, Saudi Arabia, the European Union and Japan. Russia, with an indicator of more than $400 billion, is also in the top ten. Other countries with large gold and foreign exchange reserves also include Hong Kong, South Korea and Taiwan. The countries in the second ten are Great Britain, Italy, France, Singapore, Mexico, India, Germany and the USA.